5 Super Semiconductor Stocks to Buy Hand Over Fist for the AI Revolution - The Motley Fool

🥇 Bonuses, Promotions, and the Best Online Casino Reviews you can trust: https://bit.ly/BigFunCasinoGame

5 Super Semiconductor Stocks to Buy Hand Over Fist for the AI Revolution - The Motley Fool

Many people would associate artificial intelligence (AI) with chatbots like ChatGPT or even Bard, which was released more recently by Alphabet's Google. It makes sense because the software is consumer-facing. But those platforms wouldn't exist without the advanced semiconductor hardware used to train each AI model.

In fact, investors might find that some of the greatest AI opportunities over the next few years are actually in the hardware space where companies are racing to build infrastructure to support the advanced technology.

Let's look at five stocks involved in AI's hardware space, starting with a name most investors are likely already familiar with. Image source: Getty Images. 1. Nvidia

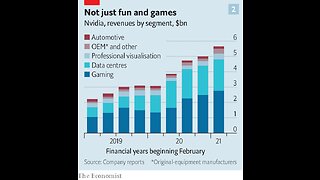

The increased hype around AI helped Nvidia (NVDA -1.90%) become synonymous with AI this year, but its history with the technology goes back much further. In fact, Nvidia delivered the first AI supercomputer to OpenAI back in 2016, and Nvidia's graphics processing unit (GPU) chips have been used to train the ChatGPT platform ever since. Nvidia CEO Jensen Huang estimates there is $1 trillion worth of data center infrastructure in use today that needs to be upgraded to support accelerated computing and AI, and his company has an estimated 90% market share in that segment.

As a result, the world's largest cloud providers are rushing to get their hands on Nvidia's hardware, but some have also partnered with the chipmaker to deliver its DGX supercomputer to their customers. This will enable millions of regular businesses to access the computing power necessary to train their AI models without investing billions of dollars to build the infrastructure.

Nvidia stock has soared 190% this year and officially surpassed a $1 trillion valuation. Its price-to-earnings (P/E) ratio of 139 is over four times more expensive than the 31 P/E of the Nasdaq-100 index. So investors interested in this stock should tread with caution in the short term. But in the long run, I think Nvidia has the potential to eventually become the largest company in the world.

2. Axcelis Technologies Axcelis Technologies (ACLS -0.92%) is a far smaller company than Nvidia, with a valuation of just $5.4 billion, but its stock has more than doubled this year on the back of an incredibly strong operating performance. Axcelis doesn't produce chips; it's a semiconductor-service company that makes ion implantation equipment critical to the fabrication process.

The world's leading chipmakers will likely experience heightened demand for hardware as AI adoption continues to grow, and they'll need the equipment produced by companies like Axcelis to expand their production capacity. In fact, over the last 12 months, Axcelis received more orders than it can possibly fill, leading to a record-high backlog worth $1.27 billion.

The company generated $922 million in revenue in 2022, representing year-over-year growth of 38%, while many other chip companies were succumbing to the broader economic slowdown. This year, Axcelis expects to deliver $1.03 billion in revenue (a recently lifted forecast) as it continues to work through its order backlog.

Its stock is still very attractive because it trades at a P/E ratio of just 29.2, a slight discount to the Nasdaq-100. As a result, this could be a great time for investors to buy despite its strong gains this year already.

3. Micron Technology Micron Technology (MU -1.46%) has flown under the radar this year because investors have been focused on semiconductor producers, like Nvidia, making powerful graphics processors for AI workloads. Micron, on the other hand, is a world-leading manufacturer of memory (DRAM) and storage (NAND) chips used in everything from smartphones to data centers to electric vehicles. But Micron says AI servers can require up to eight times the DRAM content of a regular server and up to three times as much storage, so the company is likely to also benefit from the broader deployment of AI in the long run. In other words, don't sleep on the future potential of this stock.

In the shorter term, Micron is grappling with challenges in its consumer segments, which have slowed significantly because people are simply buying fewer personal computers and devices amid the recent economic slowdown. As a result, Micron found itself with...

-

7:16

7:16

Best Product Reviews

11 months agoThe Best AI Stock to Own Could Be Sitting in Your Pocket - The Motley Fool

1031 -

7:23

7:23

Best Product Reviews

1 year agoNvidia is not the only firm cashing in on the AI gold rush - The Economist

46 -

10:17

10:17

siegebreakstudiollc

2 months agoHow Did NVIDIA Became a Mega Chip Giant Worth TRILLIONS?

34 -

37:43

37:43

Kitco NEWS

2 months agoIs the AI & NVIDIA Hype Justified? What’s Next for the Stock Market? - David Nelson

321 -

8:11

8:11

Money Talk Sundayz

1 year agoTop 5 Stocks Eating Off ChatGPT, OpenAI

58 -

4:28

4:28

LumleyTrading

1 year ago$NVDA Stock Analysis - Is It Time To BUY Or SELL Nvidia???

85 -

0:58

0:58

The Last Capitalist in Chicago

11 months ago $0.01 earnedNvidia board member dumping $76 million in stock

36 -

2:28

2:28

gmketfsystems

3 months ago5 easy trades for tomorrow $NVDA stocktrades for tomorrow

28 -

15:19

15:19

StockTradingTips

7 months agoSemiconductor Stocks Battle for Market Dominance: Who Will Lead the Chip Race? | NVDA Stock Analysis

-

13:23

13:23

Finance

6 months agoAMD vs Nvidia: How to Invest in A.I and Semi Conductors to Build Future Wealth

15